Maria R. Korobeynikova,

Far Eastern State Transport University, Khabarovsk, Russia

Roman G. Korol

Far Eastern State Transport University, Khabarovsk, Russia

Abstract: The article discusses the situation on the global and Russian transport and logistics markets during the period of the transport crisis (2020-2022). It provides the analysis of challenges facing Russian participants of global international logistics. The main goal of the article is finding solutions for the development of the Russian logistics market, including alternative transportation routes via Iran and Azerbaijan. There is a comparison of traditional and alternative routes and evaluation of delivery delay risks for each of them based on a statistical method. The evaluation results are analyzed, assumptions are made about the roots and causes and possible solutions are proposed for removal of barriers hindering the cargo traffic along the proposed routes.

Keywords: border crossing point, international transport corridor, transport logistics, transport and logistics infrastructure.

A transport logistics is the most dynamic sphere of economic at the macro and micro levels. We need to consider the influence of external factors, including political, economic, social and environmental to achieve maximum efficiency of logistics processes. The previous two years are characterized by global supply chains imbalance as most of the established logistics channels have become broken or corrupted. The imbalance of global supply chains started from global pandemic in 2020 when most of the well-established transportation schemes collapsed. This led to subsequent development of the transport crisis in 2021 and per this day.

The deferred demand was the reason for global transport crisis; it emerged during quarantine restrictions. This demand was much higher than available offer at the end of 2020 and beginning of 2021, which caused the destabilization of the existing supply chains. The main reason of such a deferred demand was quarantine restrictions imposed during the period of the 2020 pandemic. According to quarantine procedures if at least one person tested positive for COVID-19, the logistics terminal had to be closed immediately. Moreover, it was prohibited to cross borders for foreign trucks. This caused a huge queue for border crossing. Another reason was the energy crisis. Twenty Chinese provinces had problems with the supply of electricity, and the government imposed restrictions on its use. This led to disruptions in the work of factories and in the shipments schedule.

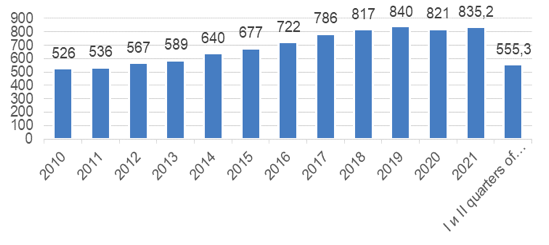

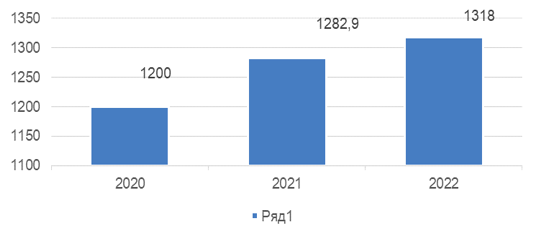

However, flexibility in responding to changing conditions and the possibility of using an alternative logistics options slowed down the consequences of the transport crisis in Russia. According to the annual reports by ROSMORPORT the decrease in the cargo turnover of the Russian seaports amounted to 2.3% million tons in 2020, however, at the end of 2021, the cargo turnover of the seaports of the Russian Federation increased by 1.7% and eliminated the 2020 decline. [1] Port cargo turnover in 2022 for the first two quarters compared to the same period in 2021 increased and amounted to 553.3 million tons (Fig. 1). [2] Rail transportation became the growth point for the Russian logistics in 2021. According to JSC “Russian Railways”, rail transit of containers increased by almost 50% in the first three quarters of the year. Thanks to well-coordinated work in this sphere, the trade turnover between the Russian Federation and China has significantly increased: by the end of 2021, it amounted to 140 billion USD, which is 30% more than in 2020. [3] The growth trend continues in 2022: 1.2 million TEU were transported through the main railway crossings of the Russian Federation with Asian countries in the period January-October 2022 (increase on 6% compared to January-October 2021). The main border crossings are Dostyk – Altynkol (China – Kazakhstan) – 593 thousand TEU, and Naushki and Zabaikalsk – 611 thousand TEU (Fig. 2).

Fig. 1. Cargo turnover dynamics (million tons) of the Russian seaports in 2010-2022

Fig. 2. Cargo turnover dynamics (million tons) of the Russian Federation railway transport in 2020 – 2022

The railway network was not ready for the additional load caused by the redirection of the cargo stream; it had a rather low throughput capacity due to outdated infrastructure. As a measure to overcome this problem, the Eurasian Union of Rail Freight Transport Participants whose members are the largest container operators in Russia, in 2022 has prepared a list of measures that allow the competent use of the existing railway capacities. A joint project of the EAEU countries named “Eurasian Agroexpress” was also developed. The latter is an accelerated rail and multimodal transportation project focusing firstly on China and Uzbekistan routes (and back). [4]

The Russian logistics market has been seriously influenced by external factors in 2022. The largest international maritime lines have begun to impose restrictions on Russian ports and supported the imposition of sanctions since March 2022. [5] Vessels and containers of the main international maritime operators could not enter Russian ports; among them are “MSC”, “Maersk”, “ONE”, “CMA CGM”, companies occupying almost half of the global market. After the European Union introduced a list of prohibited and dual-use cargoes, the processing of customs clearance in border areas began to last for weeks as it forced the customs authorities to inspect each container. After the industry leaders stopped any activities with Russian ports, there were carriers who have managed to take a share of cargo flow and strengthen their positions in spite of imposed sanctions. For example, some Turkish sea lines still accept containers in Novorossiysk; some operators continue to transport non-sanctioned cargoes from Europe to the port of St. Petersburg (“Unifeeder”).

The actual political and economic situation has highlighted the long standing problems in Russian transport & logistics system:

- The lack of carriers capable to satisfy the emerging demand for export and import shipments. The main cargo flow in 2022 goes trough Far Eastern ports, but FESCO, the principle Russian shipping operator in this basin cannot handle this cargo volume even in cooperation with “Russian Railways”;

- Insufficient number of own containers, fleet assets as well as railway rolling stock;

- An outdated port, railway and border crossing points infrastructure that is not able to take on the extra cargo turnover after the main global industry leaders left Russian logistics market;

- Complicated inspection procedures at border and customs crossings.

The transportation efficiency through the main existing channels is not predictable due to the difficulty in booking, document processing and customs clearance. Introduction of alternative logistics directions can level these problems.

It is necessary to consolidate logistics in the Eastern direction. Transportation from the eastern ports of India to the Vostochny / Vladivostok ports is becoming increasingly important now. “Vladivostok Commercial Sea Port” (part of the FESCO Transportation Group) plans to proceed 757 thousand TEU in 2022. According to the reports by this stevedoring company, the cargo turnover in the first and second quarters of 2022 increased on 7.2% compared to the same period in 2021. [6]

The directions through Iran, Turkey, Kazakhstan, and Uzbekistan are as well perspective. The main logistics corridor here is North-South direction. It originates from the Indian port of Nava-Sheva, and then goes through Iran to St. Petersburg seaport. This route makes possible to halve a transit time compared to traditional directions via the ports of Novorossiysk and the Far East.

(End of introductory fragment)